Are you drowning in credit card debt and feeling overwhelmed by high interest rates? If so, perhaps it’s time to consider a game-changing solution — the balance transfer credit card. This financial tool can help you regain control of your finances and save money on interest payments. But what exactly is a balance transfer credit card and how does it work? In this blog post we will demystify the world of balance transfers, explore their pros and cons, highlight some of the best options available on the UK market and provide answers to common questions. So buckle up as we delve into the exciting world of balance transfer credit cards!

What is a Balance Transfer Credit Card?

A balance transfer credit card is a financial tool that allows you to transfer your existing credit card debt from one card to another. This allows you to take advantage of lower interest rates or even 0% APR promotional periods that the new card offers.

This involves transferring the outstanding balance from your current credit card(s) to a new card, saving you money on interest charges. This can be particularly beneficial if you have high-interest debt and are struggling to make significant progress toward paying it off.

The process typically involves applying for a new credit card specifically designed for balance transfers. Once approved, you provide the details of your existing debt to the new issuer, who then initiates the transfer process. The old account is paid off with the new account’s funds, effectively consolidating all of your debts in one place.

While this may sound like a simple solution to dealing with mounting debt, there are certain factors to consider before diving headfirst into a balance transfer. Understanding the fees associated with transferring balances and carefully reviewing introductory offers or promotional periods are important steps in making an informed decision.

Why do people choose balance transfer credit cards? Aside from potentially reducing interest expenses and simplifying their payment schedule by consolidating debt into one manageable monthly payment, some people also use this opportunity to pay off their debt more aggressively.

However, it’s important not to think of these cards as magical solutions that will wipe out your debt overnight! They require discipline and careful planning. It is important to have a clear repayment strategy during the introductory phase and beyond.

How does a balance transfer credit card work?

A balance transfer credit card can be an effective tool for managing and reducing your debt. But how exactly does it work? Let’s break it down.

If you have multiple credit cards with balances, you can transfer those balances to one card through a balance transfer. This can be particularly beneficial if the new card offers a lower interest rate or a 0% APR balance transfer promotional period.

Once you’ve received approval for a balance transfer card, you’ll need to provide your existing credit card details and specify the amounts you want to transfer. The new card issuer will then pay out these remaining amounts on your behalf.

Once the transfer has been completed, the transferred amount will now be available on your new credit card. Ideally, this occurs during an introductory period with a lower interest rate or no interest rate at all.

To get the most benefit from a balance transfer credit card, it’s important to pay attention to the fees associated with the balance transfer. These may include balance transfer fees or annual fees, which may offset some of the potential savings from transferring your debt.

Using a balance transfer credit card requires careful planning and review of terms and conditions. However, when used wisely, it can help consolidate debt into one manageable payment while saving money on interest expenses.

What fees are associated with transferring a balance?

If you’re considering a balance transfer credit card, it’s important to understand the fees that may be associated with this type of transaction. While transferring your existing credit card debt to a new card can save you interest and consolidate your payments, there are some costs you need to be aware of.

A common balance transfer fee is the balance transfer fee. This fee is usually a percentage of the amount you transfer and can range from 2% to 5% of the total amount transferred. For example, if you transfer £2,000 and the balance transfer fee is 3%, you will incur a fee of £60.

Another possible cost factor is the annual fee. Some balance transfer credit cards may have an annual fee that must be paid each year to maintain your account. It’s important to weigh these costs against any potential savings that will come from consolidating your debts onto one card.

Advantages and disadvantages of a balance transfer card

A balance transfer card can be a useful tool for managing credit card debt, but it also has advantages and disadvantages. Here are some of the key balance transfer pros and cons to consider:

Advantages:

- Lower interest rates: One of the main benefits of a balance transfer card is the ability to transfer high-interest credit card debt to a card with a lower interest rate. This can significantly reduce the amount of interest you pay each month, allowing you to save money and pay off your debt faster.

- Debt consolidation: If you have multiple credit cards with outstanding balances, a balance transfer card can help consolidate your debts onto a single card. This can simplify your financial management since you only have to make one payment each month instead of keeping track of multiple due dates.

- Introductory offers: Many balance transfer cards come with introductory offers such as 0% APR for a specific period of time, usually between six and 18 months. This gives you a window of opportunity to pay off your transferred balance without incurring interest charges.

- Improved Credit Score: A balance transfer card can help improve your credit score over time by consolidating your debts and making regular payments on time. This is because it is responsible credit behavior, such as: B. by paying off debts and not using available credit.

Disadvantages:

- Fees for transferring the balance: Some balance transfer cards charge balance transfer fees, typically around 3–5% of the amount transferred. While this fee may be worth it if you save significantly on interest payments, it’s important to take this cost into account when considering a balance transfer card.

- Limited time for introductory pricing: The low or 0% APR introductory offer on balance transfer cards is typically only available for a limited time. After the promotional period ends, the usual interest rate on the balance transfer card applies. It’s important to understand the card’s terms and conditions, especially when the promotional price expires.

- The temptation to spend money: When you transfer your balance to a new card, it can be tempting to continue using the old card or even use the new card for additional purchases. This can lead to further debt accumulation and defeat the purpose of the balance transfer.

- Participation requirements: Not everyone is a candidate for a balance transfer card, as these cards often require good credit. If your credit isn’t good, you may not be eligible for a balance transfer card with favorable rates or at all.

It’s important to carefully consider these pros and cons before choosing a balance transfer card. Analyze your current financial situation, evaluate the terms of the card, and determine whether it aligns with your goals and ability to use credit responsibly.

How long does it take to transfer funds from one credit card to another?

The time it takes to transfer funds from one credit card to another can vary, typically between four and seven days.

The process includes:

- Applying for a new credit card

- Authorization received

- Initiation of the request to transfer the credit

- Give both credit card issuers time to process and complete the transfer

It’s important to continue making payments with the old credit card until the transfer is complete. It’s also a good idea to read the terms and conditions or contact the credit card issuer for exact balance transfer deadlines.

The best balance transfer credit cards in the UK

When it comes to finding the best balance transfer credit cards in the UK, some standout options can help you save money and manage your debt more effectively. These cards offer low or even 0% interest rates on balance transfers for a specified period of time, allowing you to consolidate and pay off your debt without incurring additional interest charges.

1. Tesco Balance Transfer Credit Card

The Tesco Balance Transfer Credit Card is a popular option for anyone looking to transfer their credit card balance. Thanks to competitive interest rates and special offers, this card can help you save money on interest payments and manage your debt more effectively.

One of the key features of the Tesco Balance Transfer credit card is its 0% introductory balance transfer period. This means that you can transfer your existing credit card balance to this card and not have to pay interest on that balance for a certain period of time. This can be particularly beneficial if you have high-interest debt that incurs significant monthly interest charges.

In addition to the attractive balance transfer offer, the Tesco Balance Transfer credit card offers other advantages. For example, you get Clubcard points for every purchase you make with the card. These points can be redeemed for various rewards or used for future purchases at Tesco stores.

It’s important to note that while the Tesco Balance Transfer credit card appears to be an excellent option, there are some fees associated with transferring a balance. These include a balance transfer fee, which is usually a percentage of the transfer amount, as well as any applicable foreign transaction fees.

If you want to consolidate your debts and save money on interest payments, the Tesco Balance Transfer credit card could be a good choice. Remember to read all terms and conditions carefully before making a decision!

Shortcut:

2. Barclaycard Platinum Credit Card

The Barclaycard Platinum credit card is one of the top options when it comes to balance transfer credit cards in the UK. With its competitive features and benefits, this card can help you manage your debt effectively.

One of the main benefits of the Barclaycard Platinum credit card is the 0% interest period on balance transfers. This means that you will not be charged any interest on your transferred balance for a certain period of time, usually up to 24 months. This can significantly reduce the amount you owe and give you time to pay off your debts without incurring additional costs.

Another great feature of this card is the low balance transfer fee. While some credit cards charge high balance transfer fees, Barclaycard offers a reasonable fee that makes it more affordable for those looking to consolidate their debt.

In addition to these benefits, the Barclaycard Platinum credit card offers access to exclusive perks such as discounted tickets to events and experiences through its Barclays Tickets entertainment platform. This can be a nice bonus if you enjoy attending concerts or shows.

Shortcut:

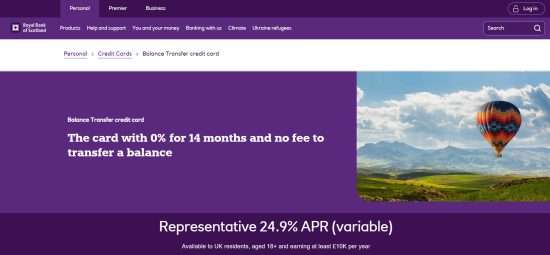

3. Royal Bank of Scotland credit card with balance transfer

The Royal Bank of Scotland Balance Transfer credit card is a popular choice for people looking to consolidate their credit card debt. With competitive interest rates and a range of benefits, this card can help you save money and manage your finances effectively.

A key feature of the Royal Bank of Scotland balance transfer credit card is the balance transfer offer. This allows you to transfer existing balances from other credit cards to this card at a low or 0% interest rate for a specific period of time. This can help you reduce the interest on your debt and make it easier to repay.

In addition to the balance transfer offer, this card also offers other perks such as cashback rewards and discounts on purchases at select retailers. These additional benefits can help you maximize your savings and get more value from your everyday spending.

To apply for the Royal Bank of Scotland Balance Transfer credit card, you must meet certain eligibility criteria, such as: E.g. good credit and residency in the UK. Once approved, transferring your credit should be a straightforward process that can be completed online or over the phone.

Shortcut:

4. Virgin Money Balance Transfer Credit Cards

Virgin Money offers a range of balance transfer credit cards to help you manage your debt more effectively. These cards allow you to transfer the balance from your existing credit cards to a Virgin Money card, saving you on interest costs and potentially helping you pay off your debt quicker.

A key benefit of Virgin Money balance transfer credit cards is their competitive introductory offer. For example, some of their cards may have an interest-free balance transfer period, allowing you to pay off your transferred balance during this time without incurring interest charges.

In addition to the attractive promotional offers, Virgin Money also offers other benefits such as reward programs and cashback incentives. These benefits can make managing your finances even more rewarding.

It’s important to note that while transferring balances can help reduce interest payments, there may be fees associated with the process.

Shortcut:

5. Santander Everyday credit card

The Santander Everyday Credit Card is a popular balance transfer credit card in the UK. With this card you can transfer your existing credit card balance and consolidate it into one account. This can reduce your interest costs and make it easier for you to pay off debt.

A great feature of the Santander Everyday Credit Card is its introductory period of 0% interest on balance transfers. For a certain number of months, usually between 18 and 24 months, you will not be charged interest on the transferred balance. This gives you enough time to pay off your debts without incurring additional interest costs.

In addition to the attractive promotional offer, Santander also offers competitive conditions for purchases with this credit card. This means you will benefit from low interest rates for paying everyday expenses even after the introductory period has ended.

Another advantage of this card is that there are no annual fees. This means that in addition to settling your outstanding balance and any transfer fees that may apply, you don’t have to worry about hidden or recurring costs.

Shortcut:

Diploma

In summary, a balance transfer credit card can be helpful in managing and reducing your debt. By transferring high-interest balances to a low- or no-interest card, you can save money on interest costs and pay off your debt faster. It’s important to carefully research and compare different balance transfer cards before choosing one that best suits your needs and financial goals. If used responsibly and making payments on time, a balance transfer credit card can help you regain financial stability.